Another Chinese promote

The Equity Dispatch #51

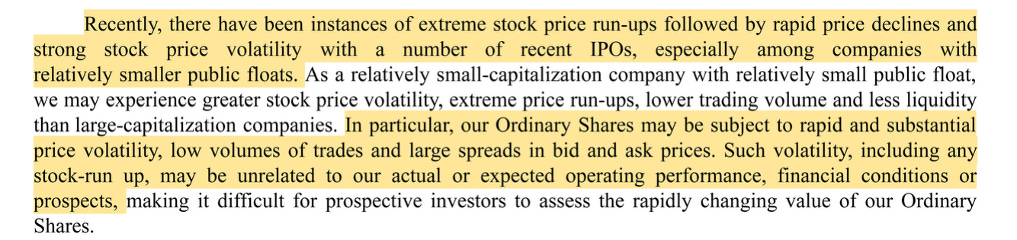

Rich Sparkle is an absurd, Hong Kong based financial printing company whose share-price rise can only be attributed to the thin float—about 10% of the company. That means that, if the 90% of under-the-surface owners chose to buy at prices higher than the company merits, a few purchases would drive up the price of the whole company. We do not know whether this stock is manipulated, but there is nothing we can identify in the fundamentals or the sector it operates in that would make ANPA an attractive company to own at its current valuation. The company’s own filings prophetically describe this situation:

As of September 29, ANPA has risen over 7x since its IPO July 11, 2025 and now trades at about 64x 2024 revenue and 462x profit based on the pre-IPO and extra shares issued after its offering. ANPA made $5.9 mln in revenue in 2024 and $820,393 in profit and has a market capitalization of about $379 mln. The high profit multiple comes despite a decline in revenue (but a small increase in profit) in 2024 compared with 2023. The company’s share price suggests that ANPA is a high-growth, money-printing machine. In reality, it’s a stagnant-growth financial documents service provider operating in a dull market with aspirations to grow in its existing and other dull markets.